You May Have to Dig a Little to Identify Fees in your 401k. It’s a One-Time Chore so Get Out Your Shovel!

Hi Friendos,

I’ve written about minimizing investment costs in some prior newsletters. In a 2023 newsletter, I explained that a “low cost” fund is defined by having a low expense ratio. To me, an expense ratio of 0.20% or less is “low.” In a 2025 newsletter, I got into how mutual funds and ETFs actually levy their fees. In a nutshell, they charge investors a little bit every day, and it is baked directly into the price of the fund, not reported separately on your account statements.

You don’t have to take my word for it that low fees matter. John Bogle founded Vanguard (a member-owned cooperative that is one the largest and most successful asset managers in the world, with over $11 trillion in assets under management) and he spoke about this topic all the time:

- “The More the Managers Take, the Less the Investors Make.”

- “Fund performance comes and goes. Costs go on forever.”

And here is what the Securities and Exchange Commission said about fees, in two investor bulletins published last year:

- “A fund with higher costs must perform better than a lower-cost fund to generate the same returns for you.”

- “These fees may seem small, but over time they can have a major impact on your investment portfolio. This is because fees and expenses reduce the amount of money in your investment portfolio earning a return.” (emphasis in original)

Ok, ok, you’re sold! Now you just need to know: what are the fees for the funds you could choose to purchase inside your 401k? Your employer has selected this list of funds, hopefully with an eye to low-cost index funds.

Your employer’s benefit guide, if there is one, is unlikely to provide any serious detail on the retirement plan, it will instead point to the relevant website or tell you to ask HR about it. That’s not a knock on your employer; there are so many details a person might want to know about a retirement plan, it’s not feasible to include all that in a benefits overview guide. Also, retirement plans must comply with legal disclosure requirements!

One of those requirements is to tell you the “expense ratio” for each fund offered in the retirement plan. They have to give this to you as a percentage and expressed as a dollar amount for a $1,000 investment.

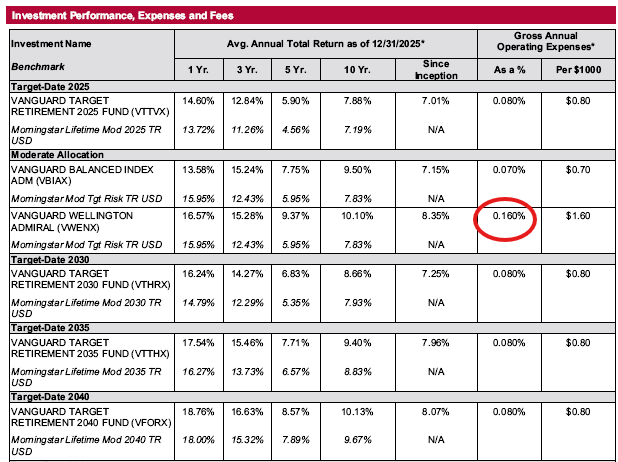

Here’s a real example of this, in the two right-most columns of the table:

See that one I circled in red, 0.16%? That’s the highest one on this page (it was a multi-page list of funds offered), and it’s the only one that’s an actively-managed fund rather than an index fund, and it has 2x the fees of the other available funds.

I found this table by browsing through the menu options on the website for this particular 403b, and it was available under “Plan Documents”:

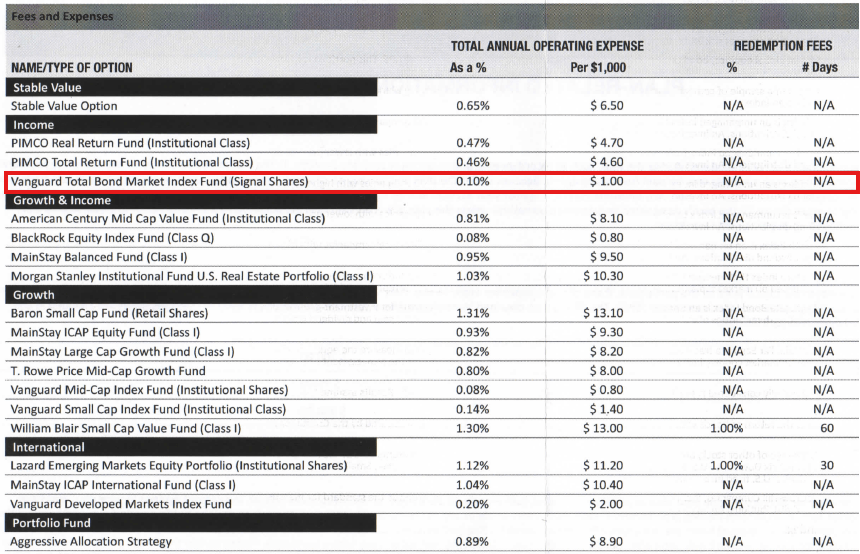

Here’s another example of fund expense ratios, from a different retirement plan, showing a much larger range of fees. I circled one of the index funds offered, which only charges 0.10% a year, compared to actively managed funds that charge up to 13 times as much:

You can see the exact wording in the two tables differs, referring to “Total Annual Operating Expense” in one table vs “Gross Annual Operating Expenses” in the other, but they refer to the same thing, which is how much you have to pay the fund manager each year. I prefer to pay less!

So now that you’ve seen a couple examples, you should be able to review your own retirement plan documents and find the equivalent table for yourself. Review the fees and if you are currently paying a lot, see if you can swap into a lower cost fund. Like I said last week, you won’t have any tax bill if you choose to do that, so don’t hesitate to make that move and save more for your future self.

-Stephanie