Hello Friendos,

This week I am thinking about debt. Partly because I’ve been reading David Graeber’s book Debt: The First 5,000 Years (excellent!) and also because of a recent conversation about how to get out of debt.

Here is my recipe:

Step 1. Decide you want to get out of debt. This mindset is key to success and I think nearly everyone who makes this decision can do it.

Step 2: Stop adding to the debt. Having a bit of savings, a mini emergency fund (like, $1,000-$2,000), is key. Whenever an unexpected required expense comes up, draw down on the savings and don’t put anything on a credit card.

Step 3. Make a list of your debts: how much is currently outstanding, to whom/what entity, current interest rate, and minimum/required monthly payments. Think about: credit cards where you carry a balance, home mortgage, student loans, auto loans/leases, personal loans, payment plans for back taxes, medical debt, etc.

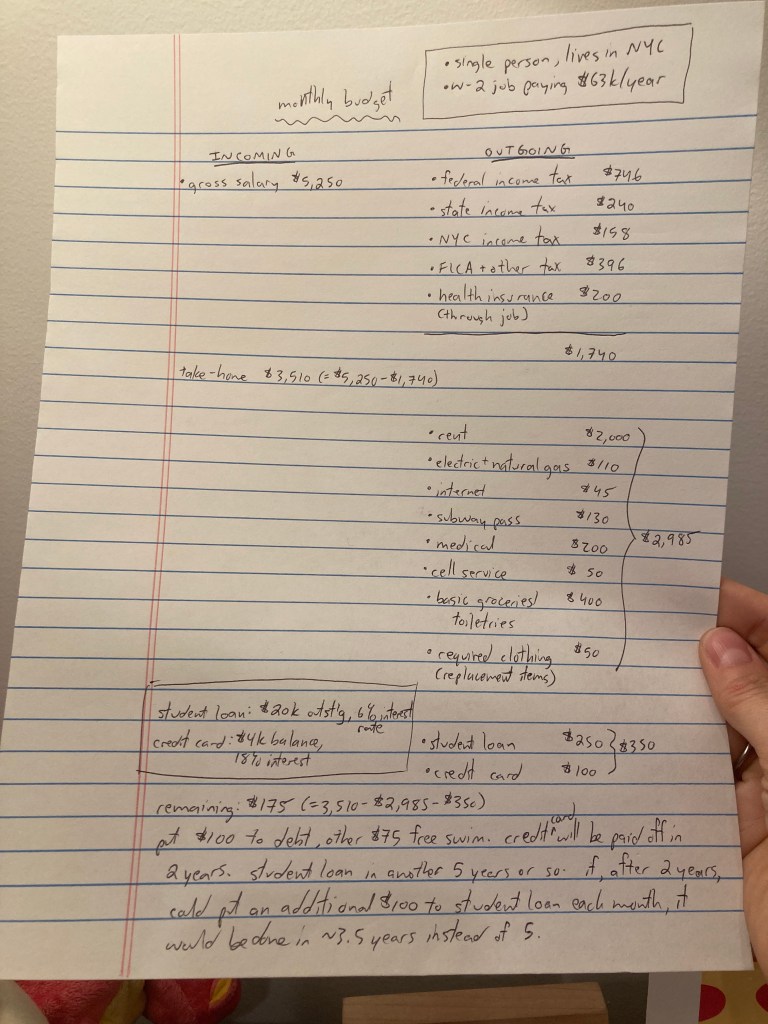

Step 4. Make a money plan (a budget) that includes debt payoff. Identify your incoming cash each month, and your outgoing cash each month. Outgoing needs to include debt pay down.

Step 5. Work the plan and adjust as needed. After each month, see how your actual spending compares to your plan. The first time you do this, you will be off, but like anything you will get better with practice. By focusing on the debt paydown, you will have ideas about how to get there faster.

The overall concepts are simple but simple does not mean easy. And some of these steps have subparts. For example:

Step 4a: Figure out your incoming cash each month. If you have a salaried W-2 job where you are paid monthly, this might take 2 minutes since you just need to look at your last paystub. If you are paid once a week or once every 2 weeks, you’ll want to convert that to a monthly amount to create a monthly budget. Do you have to budget monthly? Why not every 2 weeks if that’s how often I get paid? That’s fine too – whatever works for you. What if my income varies from month to month? You can either (1) plan based on a minimum incoming you know you’ll achieve or (2) spend this month’s income next month (you already know the exact amount that came in).

Step 4b: Plan your monthly spending. Start with basic requirement must-haves: housing, medical care, utilities, basic groceries, transportation to work. If you are self-employed, you need to set aside for taxes. Don’t forget required expenses that may be less frequent, like car insurance (depending on the billing plan), or higher in certain months (like a higher winter utility bill for heat).

Then you need to allocate to your required debt payments. Maybe you’ll use the debt snowball approach or maybe the debt avalanche. Pick whatever approach resonates with you.

Then you can plan for a bit of extras. Most prized extras are different for different people. For you it could be a gym membership, or one meal in a restaurant a week, or piano lessons for your kid, or saving for a family reunion plane ticket. It is nice to give yourself (budgeted) rewards for debt reduction milestones to keep up the motivation.

Then everything left goes to extra debt payments. Of course the less you spend on extras, the faster you’ll get out of debt. Any windfalls or extras that come your way (like a tax refund, or a raise at work) – put all of that to debt. Maybe you’ll decide to earn extra income, if only for a time, to accelerate your plan. If an unexpected required expense comes up, pay for it from the mini emergency fund and then, rather than putting extra towards debt, build up the mini emergency fund again. Then resume putting all extra toward debt.

That’s my recipe for getting out of debt. Make a plan and work the plan. It is really boring. It’s also incredible to be debt-free.

-Stephanie

One reply on “The Boring Newsletter, 4/1/2023”

[…] making a list of all the debts you have (outstanding balance and interest rate) and making a budget that includes extra debt payments. If you are debt-free but don’t know where your $ goes, I […]

LikeLike