Mother’s Day Edition: Perfection is Not the Bar in Life or Investments. Target Date Funds are Fabulous.

Hi Friendos,

This morning I rounded out my news review with a feel-good piece on people’s favorite advice from their moms, since today is Mother’s Day. I especially liked the advice along the lines of “calm down and don’t let the perfect be the enemy of the good.” Perfect usually isn’t possible and it’s not the thing to strive for in personal finance when we’re trying to have our money support our lives, not the other way around.

A recent NY Times piece on target date retirement funds (gift article link) had a scary headline, “Check Your Target-Date Fund, Especially if You Plan to Retire Soon” and an equally scary subheadline,“Their simplicity makes the funds appealing, but they could leave many workers near retirement, particularly baby boomers, short on savings.” When I read this I had just counseled a client on selecting a target date fund for their 401(k) contributions. What if my client saw this piece and thought “Oh no! If I follow Stephanie’s advice and buy a target date fund, am I screwed?”

The Times’ description of target funds is excellent: “The key feature of the funds is that they gradually move from an aggressive mix of assets that aim for growth during the investor’s working years to a more conservative, less volatile mix as the investor nears retirement — the fund’s target date. There’s no rebalancing, no funds to choose and no decisions to make. All the investor needs to do is make deposits.”

Here’s a little bit more to know about target date funds:

- They usually have a specific year in their name, like “T Rowe Price Retirement 2055 Fund,” where the year indicates about when someone plans to retire or is about when they’ll be 65 years old.

- Some of them have very low costs, some have higher costs; you need to look at the “expense ratio” to check this for any particular target date fund.

- They usually invest in other mutual funds, rather than making their own direct investments. So a target date fund has other funds inside of it, and those funds have their own investments inside of them.

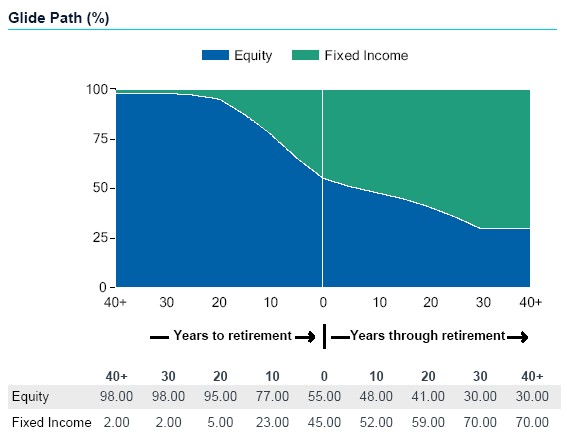

- Whether directly or indirectly, target date funds own both stocks and bonds, and as the target year approaches, they reduce the amount of the portfolio invested in stocks and increase the amount invested in bonds. The reduction in stocks (aka “equities”) doesn’t happen all at once, it “glides” down over time, so finance people call it a glide path.

Here’s an example of this from the T Rowe Price Retirement 2055 Fund:

Reading the table under the chart, I can see that for the 2055 Fund, if we check in with the Fund in the year 2045, 10 years prior to the target year, we should expect it to have 77% of its portfolio in stocks and 23% in bonds. 10 years after the target year, 2065, we should expect it to have 48% in stocks and 52% in bonds.

Sounds good, right? You don’t have to worry about portfolio rebalancing because the fund will handle that for you and you can go live your life. Well, the Times article has some critiques. Here are the specious ones, which comprise most of the article:

- The article says: “they lull workers into thinking they’re fully prepared for retirement even when they aren’t saving enough,” and “workers [may think] they’re adequately providing for their retirement, when they’re likely to end their working days without nearly enough savings.” I say: most people save too little, but that’s unrelated to the investments they select when they do save.

- The article discusses target date funds that own stocks when they reach their target year (e.g., 40% stocks or 60% stocks): “Either one of those final mixes means the fund could take a sizable hit during a big market drop.” That’s correct, stocks can go down, but that’s not some special critique of target date funds, that’s true for any mutual fund or ETF that owns stocks. If you think an appropriate asset allocation at age 65 is 0% equities, you have a critique of standard financial planning advice, not a critique of target date funds.

- The article says: “A bigger problem with target-date funds is that many investors don’t know how they work.” The reporter cites a survey with findings including, “Nearly 40 percent [of 1,500 people surveyed] didn’t know they were invested in target-date funds or thought their employer’s plan didn’t offer them.” That’s a critique of people, not target date funds.

- Finally, we have this: “the fixed glide path can limit gains for investors, experts say… ‘The fund managers have their hands tied,’ said Michael Crews, chief executive of North Texas Wealth Management in Allen, Texas. ‘They can’t say: ‘Hey, this stuff doesn’t make sense right now. This is the time to pull back on risk.’” That’s right, if you are not going to time the market, you will not gain from timing the market if, with hindsight, it turns out that by correctly timing the market you would have made more money. That is true for every passive investment, like index funds, and is not a special critique of target date funds.

There is one interesting issue that the article kind of glances on but does not explore, which is that there are large differences across these funds in their asset allocations and how they change over time, and these differences can have a big impact on investor outcomes. One target date fund might have only 40% of its portfolio in stocks by the target year while another has 65% in stocks. Similarly, the extent of non-US investment may vary substantially from one fund to another.

Asset allocation is an issue every investor must grapple with, not something specific to target date funds. Research on the ideal allocation is developing all the time (Vanguard provides a thoughtful discussion of its own approach, if you want to really dig into the topic), but we are all left making the best decisions we can under uncertainty, and we must live with knowing that the truly “perfect” portfolio can only be known after the fact.

Even the critical NY Times article with the scary headline concedes, “Even the harshest critics of target-date funds say they are better than nothing and are preferable to people picking their own 401(k) investments.” They cite a study showing that “401(k) participants who put all their money in a single target-date fund gained 2.3 percent more annually than participants who selected other types of funds in their employer plans.” Scoreboard: target date funds for the win!

If you’re my client I’ve encouraged to buy target date funds, I hope you still feel confident in that choice! Thank goodness we don’t need to be anywhere near perfect to have success in personal finance.

-Stephanie

One reply on “The Boring Newsletter, 5/10/2026”

[…] If you don’t indicate an investment, some employers will default you into a good choice, like a target date fund that is appropriate to your age. Others, however, are super conservative and will default you into […]

LikeLike