Hi Friendos,

If you work as an employee, you should have received your W-2(s) by now, which will help you file your tax return. If you’ve ever looked at a W-2 and felt uneasy at seeing a bunch of different numbers about your own income that you don’t really understand, today’s newsletter is for you. Today’s discussion can also help you better understand tax policy discourse, like this statement from a think tank article:

“The exclusion of [health insurance] premiums lowers most workers’ tax bills and thus reduces their after-tax cost of coverage…[but] the open-ended nature of the tax subsidy has likely increased health care costs.”

On the other hand, maybe you are not fussed by seeing different wage numbers on a W-2, and secretly suspect that all tax documents are sprayed with chloroform. If so, this article is probably not for you!

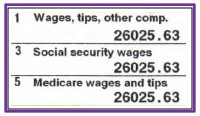

If you’re still with me, let’s dive into it with a snapshot of wage numbers on a W-2:

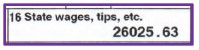

This person earned $26k and that same number is reported three times. Actually, box 16 on the W-2 reports state wages and repeats the same number a fourth time:

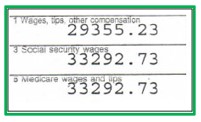

Here’s a different W-2 with $29k in wages shown in box 1 vs $33k shown in boxes 3 and 5:

And box 16 shows the same $29k number as box 1, so we have two different wage numbers, each reported twice:

I can also add, for both this green-outlined W-2 and the purple-outlined one above, none of the reported wage numbers exactly match the person’s annual salary!

When it comes to taxes, there is no single number for “income” and not every dollar is taxed the same way. The two most common things that cause differences in W-2 and salary numbers are (1) contributions to traditional retirement plans and (2) fringe benefits like medical insurance.

Culprit #1, traditional retirement plan contributions: When you contribute to a traditional retirement plan, like a 401k or 403b, those wages are not subject to federal or state income tax but they are subject to Social Security and Medicare taxes. Looking back to the green-outlined W-2 above, box 1 differs from box 3 by $3,937.50 (=$33,292.73 – $29,355.23). This difference is entirely explained by 401k contributions, as reported in box 12 with code “D” for 401k elective deferrals:

The IRS explains: “An elective deferral, other than a designated Roth contribution (discussed later), isn’t included in wages subject to income tax at the time contributed. However, it’s included in wages subject to social security and Medicare taxes.” The “tax advantage” of contributing to a traditional retirement plan is all about federal income taxes, not payroll taxes.

Culprit #2, fringe benefits: Payroll deductions for fringe benefits, like when you pay premiums for medical insurance out of your paycheck, usually cause your stated salary to differ from taxable wages. Some common fringe benefits (aka, “Section 125” or “cafeteria” plans) are:

- Dependent care FSA, where you can use pre-tax income to pay for something like child care,

- Medical FSA, where you can use pre-tax income to pay for qualified medical expenses,

- Medical insurance (also dental and vision), where you pay premiums out of your paycheck, and

- HSAs, another way to use pre-tax income to pay for qualified medical expenses.

Regarding benefits like medical insurance, the IRS explains: “In most cases, the value of accident or health plan coverage provided to you by your employer isn’t included in your income.” When part of your income goes to pay for medical insurance, or these other fringe benefits, that income is not subject to federal income tax, Social Security tax, or Medicare tax.

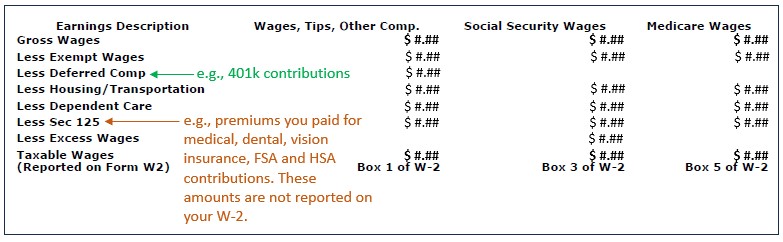

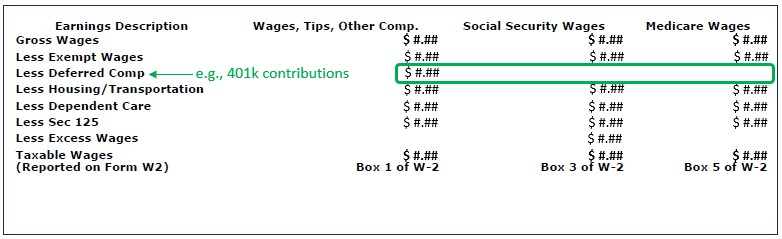

These fringe benefit amounts are not reported on your W-2, but they do cause a difference between your stated gross salary and wages reported on your W-2. Many W-2 mailings helpfully include a summary table like the following:

Each column of the table reconciles gross wages to what is reported on the W-2. Note that the second and third columns for Social Security and Medicare don’t have anything present in the row for retirement plan contributions:

That’s because those contributions reduce income subject to federal income tax, but don’t impact income subject to Social Security tax or Medicare tax.

It’s also possible for states to treat things differently than the federal government, which is why W-2’s need a separate box to report state wages (box 16). Example: New Jersey counts the income you use to pay medical insurance premiums as taxable income, so W-2 state wages (box 16) will often exceed federal wages (box 1). NJ then allows these amounts as a medical expense deduction.

One last element to consider is that some employer benefits can cause gross wages to be higher than stated salary. Example: your employer has a group life insurance plan where you don’t have to pay the full premiums. As the IRS states, “you must include in income the cost of employer-provided insurance that is more than the cost of $50,000 of coverage reduced by any amount you pay toward the purchase of the insurance.” If you are salaried and observe that gross wages on your W-2 summary are a bit higher than your stated salary, a group life insurance plan could be the reason. You can look at one of your paystubs to confirm.

I hope that demystifies any differences in wage numbers on your W-2s. Happy tax filing!

-Stephanie

One reply on “The Boring Newsletter, 2/2/2025”

[…] we need to report the amount of wages subject to Social Security tax in its own box is because it can be different from your total overall wages and different from the amount of your wages subject to other […]

LikeLike