Hi Friendos,

If you’ve been reading this newsletter for a while, you’ve heard me say things like “charitable donations probably have no impact on your taxes (so just decide what’s best for you on the merits).” I was discussing the fact that most people take the standard deduction on their taxes, and do not itemize, so they receive no tax benefit from itemizing charitable donations. I was imagining someone who gives cash to a charity (writing a check or donating via debit card or credit card).

But there are some other ways to make charitable donations in a tax-beneficial manner.

Strategy #1: Give qualified charitable distributions from your IRA.

If you have an IRA and are over age 70.5, you can give to charities, in small or large amounts, via “qualified charitable distributions” that will count toward required IRA minimum distributions. The annual max for 2024 is $105k; this amount is indexed to inflation. Typically, withdrawals from an IRA, including required minimum distributions, are counted as taxable income. Qualified charitable distributions do not count as taxable income. So, if you were going to donate anyway, and if you have to take a withdrawal from your IRA anyway, I suggest you do it this way and lower your taxable income in the process.

Strategy #2: Bunching.

If you are giving more significant amounts, consider bunching two or more years of donations into one calendar year. For example, if you typically give in December, hold off on donating until January of the following year. That way, you’ll have two years’ worth of donations taking place in one calendar year. This might change your tax math such that itemizing is better for you, and you would get a tax benefit from direct cash donations to charity.

Strategy #3: Donate appreciated investments.

Instead of giving cash, you could give some of your investments to a charity. This could be shares of publicly traded stock, shares of a mutual fund or exchange-traded fund, or another type of investment. Non-profits will typically sell the investment right away, because they are in the business of fulfilling their charitable mission, not in the investment management business.

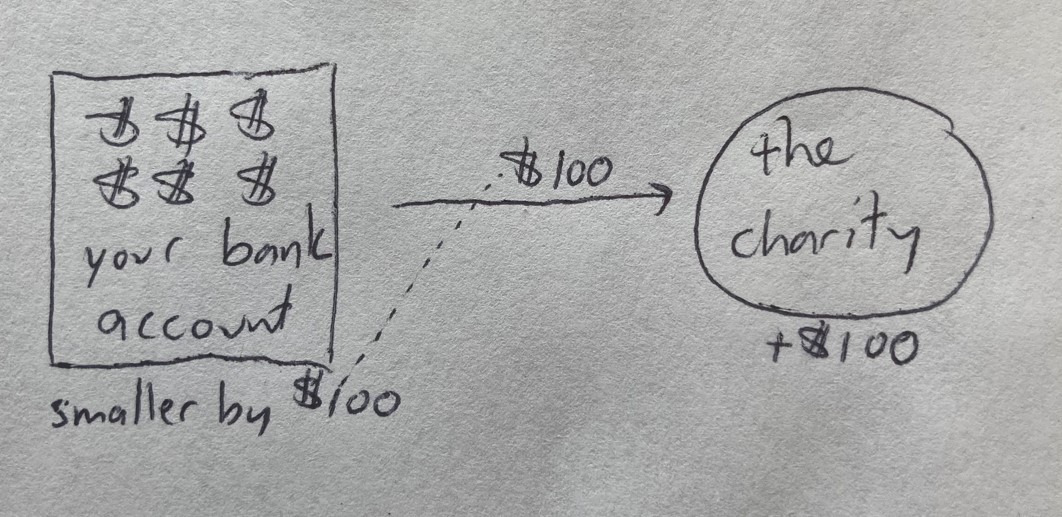

If you don’t itemize your federal income taxes, the value of the investments you donate do not reduce your taxable income, but you can use this strategy to flush out capital gains from your investment portfolio. Consider this diagram of a cash donation to a charity:

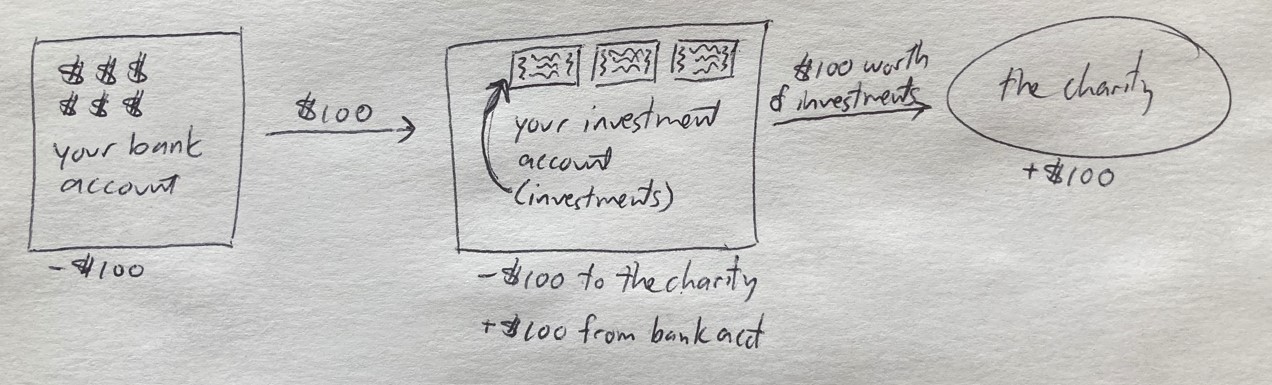

Now consider this alternative, where you donate $100 worth of an appreciated investment, and, at the same time, purchase $100 of that same investment you donated:

Why bother doing it this way? If the investment you donated was originally purchased for $60 and rose in value to $100 while you owned it, you have embedded capital gains of $40. If you sold the investment for cash, you’d have to pay tax on those $40 of gains, either at income tax rates if you held for less than a year, or at your long-term capital tax rate if you held for more than a year. That would be $6 at a long-term capital gains tax rate of 15%.

Donating appreciated investments while simultaneously buying those same investments at their current value (1) puts you and the charity in the same financial position as if you had simply donated cash, (2) flushes capital gains out of your portfolio, and (3) does not change the overall allocation of your investment portfolio.

One consideration of this strategy is that not all charities accept investments as donations. This is because they are much more time consuming to process than cash donations. Some financial institutions do a great job of communicating with non-profits, others do not. The cost of labor for the non-profit to process your gift is real. Unless your donation of stock or other investments is at least a few thousand dollars, the organization may be better off with a cash donation.

Let’s scale up my example above, so that rather donating $100 with $40 of embedded capital gains, saving $6 on your taxes (clearly not worth any administrative hassle), you are donating $1,000 with $400 of embedded gains or $3,000 with $1,000 of embedded gains. What amount of administrative hassle is worth it to save $60 or $180 on your taxes? If you can afford to donate $3,000 to charity in a year, $180 might not be much to you. The math looks different and more worth the hassle at higher amounts (e.g., donating $30k with $1.8k embedded gains).

Strategy #4: Use a donor advised fund.

This might sound like something only for the ultra-wealthy, but can be a great strategy for lots of people. If you are giving several hundred $ a year or more to charities, this one might be for you.

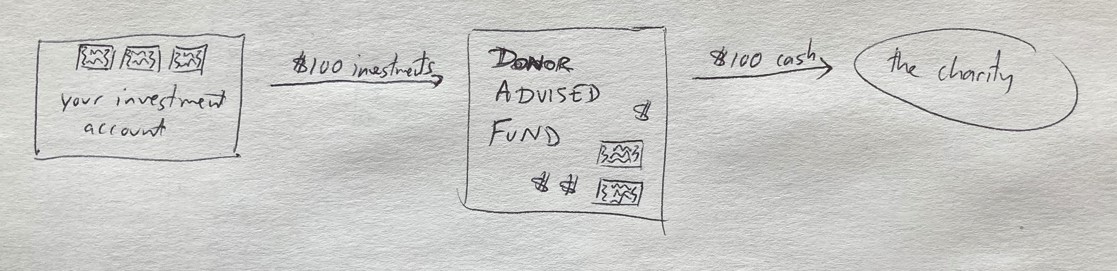

This works the same way as strategy #3, but there is the added step of running donations through a donor advised fund. I use Fidelity for my donor advised fund because it has low fees (starting at $100/year) and lets me make gifts as small as $50. It looks like this:

My diagram does not show the part where you would also add $100 to your investment account from your bank account, but I know you can imagine it!

To me, there are added benefits from using a donor advised fund (“DAF”). (1) After I put my donated investments into the DAF, the DAF can sell them and donate cash to the charities. No guilt on my end for imposing a higher processing cost on the non-profit so I get a tax benefit for myself. (2) Directing a DAF to make a grant to a charity is very easy, all done online in a few minutes. Donating appreciated investments directly to a non-profit can be administratively easy, or can be a hassle, depending on how well the non-profit is set up for that kind of thing. (3) You can have a DAF make recurring gifts. (4) No fuss wrangling a ton of tax receipts come tax time – it’s all right there in statements from the DAF.

If this intrigues you, you’ll find lots more information about donor advised funds online. I have had a great experience using Fidelity for this.

Strategy #5, DAF + bunching.

Combine use of a donor advised fund (strategy #4) with bunching (strategy #2). Let’s say you come into a windfall, like an inheritance or a big bonus at work, and would like to use that money to fund multiple years’ of charitable donations. If you contribute a bunch of investments all at once to a donor advised fund, you get to claim that full amount on that year’s tax return (this assumes you’ve held the investment more than a year – short-term investments don’t qualify). You can then have the DAF make grants over the time period of your choosing.

Personally, I don’t like the idea of big amounts being sequestered in a donor advised fund, as my favorite non-profits really need money right now. But when the money will flow out to non-profits within a couple of years, that seems reasonable to me.

I think it is very important to give to charities when you can afford it. I budget a certain % of my income each year for donations.

-Stephanie

2 replies on “The Boring Newsletter, 7/7/2024”

[…] because most people do not itemize on their tax return. That said, last year I wrote about 5 strategies to make charitable donations in a tax-advantaged way. If your giving is at a higher level, consider if these strategies might be a fit for you. If you […]

LikeLike

[…] Consider tax gain harvesting and tax optimization with charitable contributions. […]

LikeLike