Hi Friendos,

Today I want to talk about fruit. Specifically, the expression “apples to apples” and how it relates to investments, taxes, and risk.

I am inspired by a recent article in the New York Times, “Keeping a Mortgage After 65: A ‘No Brainer’ or a Big Risk?” One person interviewed said it was a no brainer for him to keep a mortgage. He said: “The money I’d have to take out of my savings or out of my investments is yielding higher interest than the interest I’m paying on the loan.” Oh yeah?

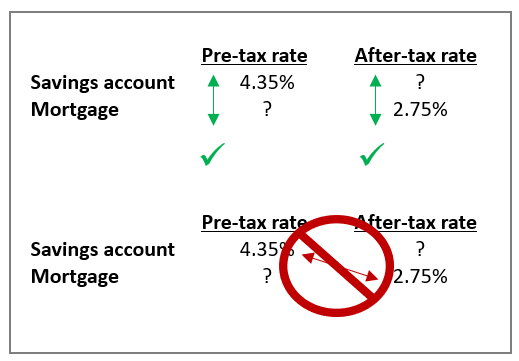

Let’s start with his savings account and assume it earns 4.35% – that’s what Ally is current paying. The article said his mortgage rate is below 3%, let’s assume 2.75%. Earn 4.35%, pay 2.75%, he pockets the difference of 1.6%, right? No! It’s not an apples-to-apples comparison without accounting for taxes.

His mortgage rate is an after-tax rate because he pays it out of after-tax dollars. Think about having a W-2 job – you can only pay your bills from your take home pay, where you employer has already held back some money for tax withholding. Investment firms and banks don’t withhold from your earnings – sometimes you can request this, but it’s not a default. The interest rate you earn on a savings account is a pre-tax rate. To directly compare this to a mortgage rate, we first need to transform it into an after-tax rate. Or, we could transform the mortgage rate from after-tax to pre-tax. We want to compare pre-tax rates to each other, and after-tax rates to each other, but not mix and match.

To fill out our table above, we need to know this man’s tax rate (federal and state combined) and use the following formula:

Pre-Tax Rate * (1 – Tax Rate) = After-Tax Rate

Simple example: say I earn 10% pre-tax, and I have to pay 30% in taxes. I earn only 7% after-tax.

10% pre-tax rate * (1 – 30% tax rate) = 10% * 70% = 7% after-tax rate

But there is not one single tax income rate – we have marginal tax brackets. So which rate should we use? Here, we are evaluating whether to keep the mortgage or pay it off, while keeping other parts of financial life the same. This is a decision at the margin so we should use the rate of this fellow’s top marginal tax bracket. I agree with Michael Kitces that “marginal tax rates should be used to compare [financial planning] strategies.” Kitces’ article is a great deep dive on this topic if you want to go further.

The news article said our 80-year-old man is married and lives in California. Let’s say he and his spouse had federally taxable income of $130k in 2023. Their standard deduction is $30,700 so they owe federal income tax on $99,300 (=$130,000 – $30,700). For 2023, that puts them at the low end of the 22% federal income tax bracket, which applies to income from $89,450 to $190,750.

The 2023 California standard deduction for a couple married filing jointly was only $10,726, so this means they have California taxable income of $119,274 (=$130,000 – $10,726). That puts them in the CA marginal tax bracket of 8%.

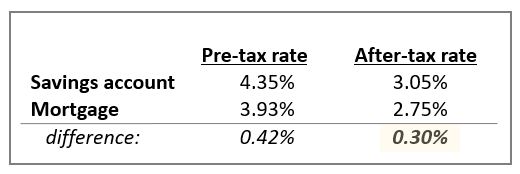

Taking their federal + state marginal tax rates we get a total of 30% (=22% + 8). So now we can fill in our table:

That difference in after-tax rates of 0.30% is what our man really pockets by keeping money in his savings account rather than paying down his mortgage. Earnings on your savings account aren’t all yours – taxes take their slice.

So you may agree that less than one third of a percent is not much to get excited about, but also: “Stephanie! This man might have a lot less taxable income than what you assumed! And what if he lives in a state with no income taxes at all?” I say: Yes! Each person needs to run the numbers that apply to their own situation.

You might also be thinking that I forgot to analyze his investment account, which he mentioned also earns a much better rate than what he pays on his mortgage. Maybe it earns something like 7% a year on average (he owns stocks and bonds). Surely that beats 2.75% even after taxes? Absolutely. Let’s say his investment are held mostly in tax-sheltered accounts like 401k accounts (realistic) and a little bit in regular (taxable) brokerage accounts. He has to pay income taxes on amounts from a 401k and capital gains tax on amounts from regular brokerage. Maybe that ends up being a blended tax rate of something like 15% or 25% — it really depends on the specifics. Average pre-tax investment returns of 10% turn into something like 6% or 5.25% after taxes. Still quite a bit more than the 2.75% mortgage rate.

But what about risk???

Savings accounts and mortgages are sure things: if you pay down your mortgage, the bank will reduce your principal balance and you will avoid paying interest in the future. If you leave money in a savings account, the bank will pay you the promised rate of interest on it. The risk is comparable. If you invest in stocks and bonds you sometimes have positive returns (even over 20% in great years), you sometimes lose money (even more than 20% in terrible years), and you never know in advance what it’s going to be. It is risky.

There is no one formula used to calculate risk-adjusted returns – there are many ways people look at this. The point is that if you earn 7% on your investments, you need to adjust for taxes and risk before comparing to other rates of return. A 7% risky return cannot be directly compared to 2.75% risk-free return.

Someone who has a paid off home cannot be foreclosed on. Even if their stock portfolio tanks. The right amount of risk is not a “no brainer” – it is something to carefully consider so you do what is right for you. Only an arrogant fool would ignore risk.

-Stephanie

p.s. hope everyone who wishes is having a very wormy weekend.

“The proximity of a desirable thing tempts one to overindulgence. On that path lies danger.”

― Margot Lady Fenring, Dune