Hi Friendos,

Last week I claimed that “nobody advertises boring” when it comes to personal finance. This week I want to talk about something that is advertised: overly complicated investment portfolios. I’m going to pick on Wealthfront because it has such a pretty website, but it’s just one example among many. First, Wealthfront wants you to know that what they do is complicated:

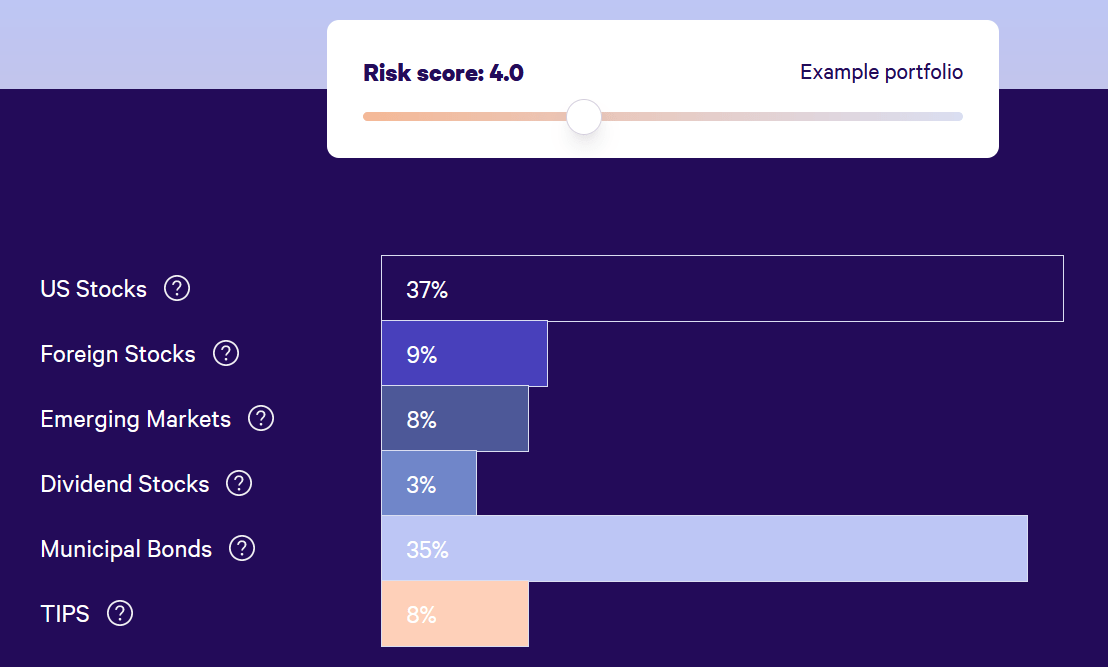

Look, probably you wouldn’t understand it, but they’ll try anyway. Also, they’ll do what they said they would with your money (was there was an alternative on the table???) so you should feel confident. Here is an example portfolio Wealthfront could build for you:

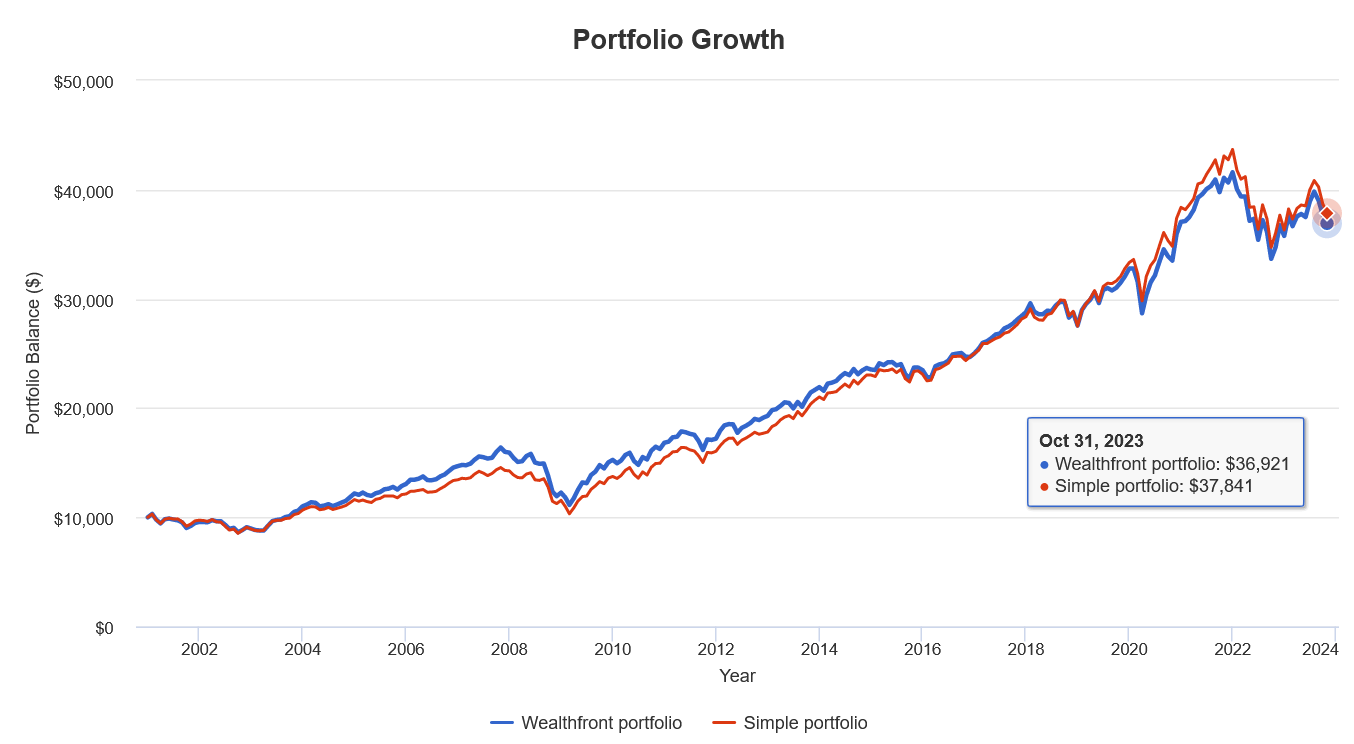

It has 6 different investment categories. I looked at this list and saw: 4 kinds of stocks (the top 4 bars in the chart) and 2 kinds of bonds (the bottom 2 bars in the chart). What if I just had one investment for stocks and one for bonds? I ran a comparison of portfolio performance using an online tool called Portfolio Visualizer. I put 57% in US stocks and 43% in US bonds, the same overall stock-bond allocation as Wealthfront:

If I invested $10,000 in 2001 in the Wealthfront portfolio, I’d have $36,921 by now. My “simple” US-only portfolio would be worth $37,841. Over a more than 20-year period we end up with 2.5% more in the US-only portfolio because it happens that overall US stocks outperformed these classes of international stocks over this specific time period (could have gone the other way).

U.S. publicly traded companies generally do business all over the world. And large public companies based in other countries generally do business in the U.S. If you have a lot of holdings in your portfolio to achieve maximum diversification or want to “tilt” your portfolio in one way or another because you think that’s better, great. If you use Wealthfront and are happy with the services, great! But if you want to keep it super simple (and swerve on paying 0.25% in annual fees to Wealthfront), I think that’s totally fine.

I hate advertising tactics that try to make people feel dumb, as if investing has to be complicated, or like people had better pay for a lifetime of help because they can’t do it on their own. This is not new to robo-advisors or investment apps. Years and years ago a friend talked to me about his investments when we were a few years out of school. He had an expensive investment advisor (his parents’ “person”) who got him into a portfolio with about a dozen different mutual funds in it. I didn’t understand why all that was necessary back then and I still don’t understand it now.

I say: focus on things in personal finance that really move the needle where you have some control/influence, like how much you earn, how much you save, actually investing your savings, and minimizing taxes and other costs. Don’t feel like you need to deep dive (or pay for help) on smaller things unless you enjoy that activity.

-Stephanie