Hi Friendos,

This week’s topic is vesting and 401k matching. It sounds so sartorial.

I’m going to walk through a very detailed (and boring) example of this with a 401k. This is a long one, so stay with me now!

Setup:

- You start a new job where your annual salary is $60,000 ($5k/month before taxes).

- To figure out what you will contribute to the 401k, you start by considering the max $’s you could put in (determined by federal law). In 2023 this is $22,500 for someone under age 50 and $30,000 for age 50+ (these #’s change a bit each year with inflation). Considering your $60k salary, this max is well above what you could realistically contribute – ok.

- Then you think about what your contributions mean for your take home pay and overall budget. You use an online paycheck calculator to play around with different contribution amounts.

- You also think about what puts you on track for a solid retirement nest egg. You are aiming to stop working in your 60s and have been doing some saving already. Something like putting away 10-15% of your gross income will work well.

- You decide to contribute $7,200 into the 401k by the end of the year (12% of your gross salary), which is $600 per month (=$7,200/12). Let’s say you get one paycheck per month.

- At some companies, 401k paperwork asks what $ amount you want to put in each paycheck. Some paperwork asks how much in % (of gross salary). Either way you’ll be able to fill out the form now.

The matching part:

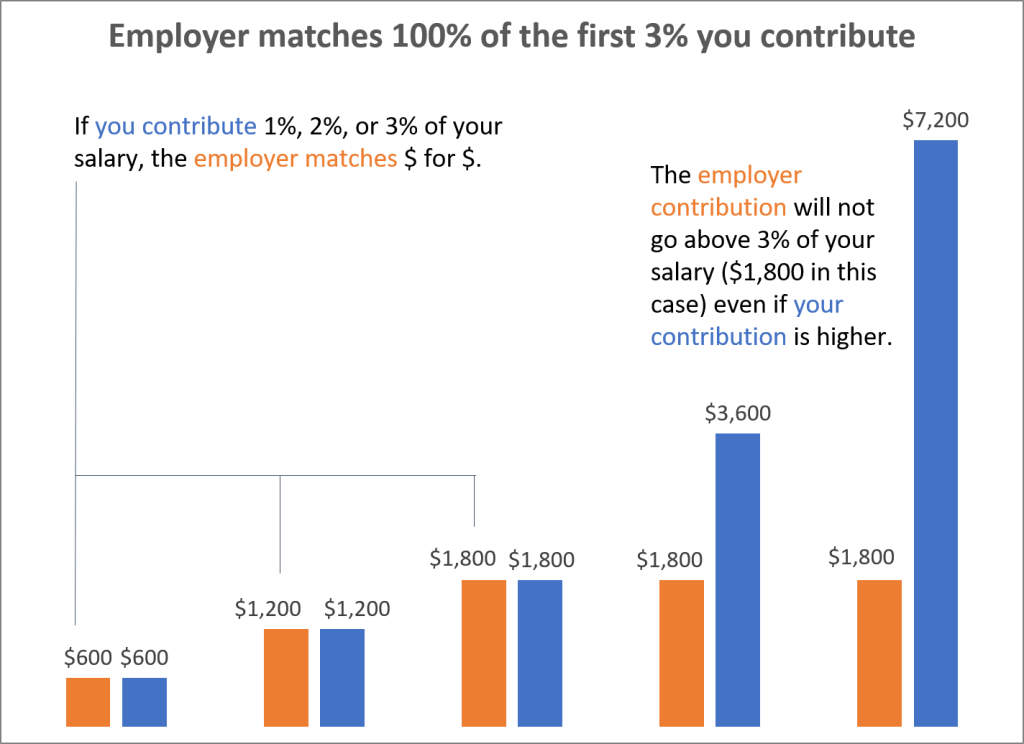

- Your employer offers 3% “matching” for the 401k plan where they match 100% of what you put in up to 3% of your gross salary. This will be the same across all employees (not, for example, a higher matching % for management than for other workers, or the plan might fail certain tests to ensure the plan does not discriminate in favor of highly paid employees).

- For you, matching 3% of your salary means matching up to $1,800 for the year ($150/month). If you put in less, so will your employer. If you put in more, your employer will still only put in $1,800. Here’s a picture:

So with this particular matching formula and your given salary, you only get the “full match” (all $1,800) if you put in at least $1,800. That match of $1,800 is part of your compensation – never leave that on the table because wouldn’t you rather be paid $61.8k (instead of $60k) for doing the exact same work?

Matching formulas are not all the same. Here’s what it would look like if the employer matched 50% up to your first 6% contributed:

- Do I think someone is overdoing it by putting in more than required to get the full match? No! This is America – putting aside 3% or 6% is unlikely to be enough (trust funds aside).

- There are some wonderful employers out there that contribute to your 401k regardless of whether you contribute, meaning they don’t “match” – they just contribute. Bless them.

- Interesting detail: the laws that govern 401k’s cap the $ amount of salary on which matching can be calculated, so if someone has a salary of $1 million a year and the 401k offers 3% matching, they would not get $30k of matching $ put in their account. In 2023, the max salary on which matching is calculated is $330,000.

Ok, so you started your new job and filled out the paperwork. You get your paycheck and see the $600 came out just like you wanted. (You did do a paystub analysis, right?) What about the $150 from your employer? Sometimes that’s shown on a paystub, sometimes it’s not. Either way, you should figure out how to log into your 401k account and, within a few business days after your paycheck drops, you should see both your $600 and the $150 from your employer in your account. The $600 might be called “employee deferral” or “employee contribution.” The $150 might be called “employer match.”

Now what? Both chunks of money will flow into whatever investment(s) you selected – that’s also part of setting up your 401k contributions. If the investments go up (or down), both the $600 chunk and $150 chunk will go up (or down).

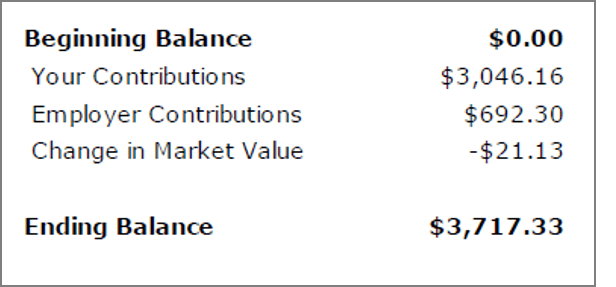

Here is a real example from when I started one of my old jobs:

My beginning balance was $0. I put in a total of $3,046.16 during this multi-month period. My employer matched some of what I put in – they put in $692.30. All of this was invested in mutual funds when the money went into the 401k account, and during this period, those mutual funds went down in value by $21.13. Beginning balance of $0 + the $3,046.16 I put in + the $692.30 my employer put in – $21.13 drop in market value = ending balance of $3,717.33.

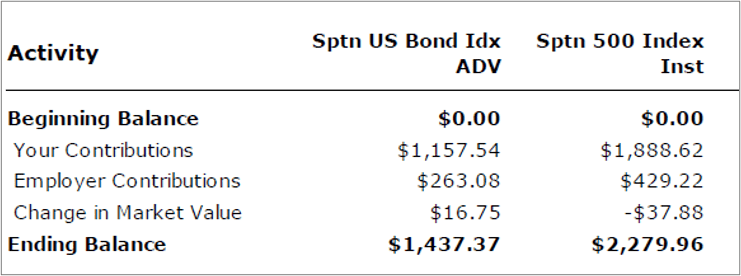

Here’s a more detailed version, showing how I chose to invest some of the contributions into a bond index fund (the left column) and some into a stock index fund (the right column). This 401k was with Fidelity and I chose these two mutual funds from what used to be named their “Spartan” series of index funds:

You can see the break down by mutual fund and across what I put in vs. what my employer put in. The bond fund gained a little bit during this period and the stock fund lost a little. Those gains and losses relate to my contributions and to the employer contributions because they were both invested in these same two mutual funds that changed in value.

So that $16.75 gain in the bond fund? There was $1,420.62 invested in the bond fund in total: $1,157.54 from my contribution, $263.08 from the employer contribution. My contribution was 81.5% of the total (=$1,157.54 / $1,420.62) and the employer contribution was 18.5%. This means that $13.65 of the gain is related to my contribution (=81.5% * $16.75) and $3.10 is related to the employer contribution. Similarly, the loss of $37.88 in the stock fund can be assigned 81.5% to my contributions ($30.87) and 18.5% to employer contributions ($7.00).

As time goes on, more contributions flow into the account with each paycheck and are invested in whatever way you chose. There will continue to be a breakdown of which amounts came from your contributions vs the employer contributions.

The vesting part:

- When an employer contributes into your 401k account, that money is not necessarily all yours right away. The part you contributed – that’s always yours.

- An employer can choose to have all the employer contributions belong to you right away. You would be “fully vested” from day 1.

- An employer can choose to set up a “vesting schedule” whereby the employer contributions become yours over time. For example, you could have 1/3 vest after your first year of service (after you’ve worked there for one year you would be “partially vested”), an additional 1/3 vest after your second year of service, and the last 1/3 vest after your third year of service.

- The vesting schedule could be 20% a year over five years. It could be 1/3 after one year and the rest after the second year. It’s totally up to the employer.

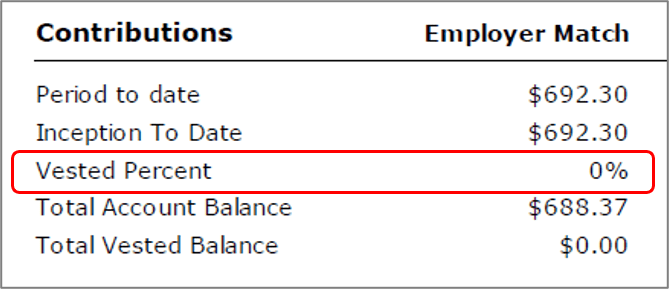

Continuing the example from my own 401k, here’s another table from my old account statement:

I’d had the job for less than a year at that point, so I was not vested in any of the employer contributions. That meant if I quit the job at that time, I would not actually get to keep $688.37 of what was in my 401k account (the employer contribution piece of it). I only would keep the part of the account related to my contributions.

A vesting schedule is possible in other areas too, like pension plans and employee stock options. If you are planning to leave a job and are not fully vested in a 401k or other area, you might want to consider if you are close to a vesting date and want to stick around until after that date.

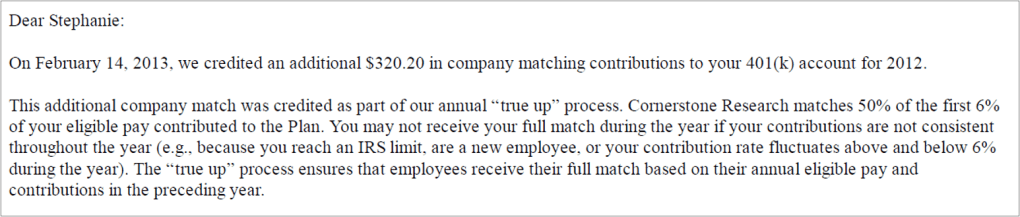

That’s how matching and vesting works. For those of you still reading, I will leave you with one last tiny boring detail on 401k matching. Matching happens with each paycheck, not all at once at the end of the year. So it is possible to end up in a situation where the employer match falls short of the amount you would calculate looking at your contributions for an entire year. This is a real email I received from a former employer:

Not all employers do a “true up” like this, and even for those that do, you generally need to still be working at the company at the time of the true up process for them to send you the additional employer contribution. For this reason, and for steady monthly budgeting, I like to make my 401k contributions evenly throughout the calendar year.

-Stephanie