I learned that a provider who “takes my insurance” may not be “in-network”

Hi Friendos,

Today I am sharing how I’ve ended up, over the last couple decades, paying a lot more for dental care than I needed to. I’ve always tried to be a careful steward of my money but my ignorance of how my insurance worked really cost me. Recognizing this now, I am getting educated and will share my findings with you!

My current dental insurance is a PPO, just like the plans I’ve had in the past. That means I can utilize my insurance benefits at both in-network and out-of-network providers, but risk being charged much higher prices if I go out of network. I don’t have any special dental needs, so I’ve always been fine with going to an in-network dentist.

After getting set up with my new dental insurance at the beginning of the year, I called my long-time dentist’s office to make sure they took my new insurance. Yes, they told me, we take your insurance. Great! I went in for my previously scheduled cleaning.

Last week I wrote about learning that only one dentist in this practice is in-network for my current insurance, and since a different dentist did my routine exam last spring, that explains why I was billed much more than the in-network rate: $575 billed vs the in-network rate of $244 for a routine exam and cleaning. My insurance covered $475 of the amount billed and my explanation of benefits (“EOB”) shows I owe $100. The dental practice never billed me for that $100. Hmm…

Because I am still within my $2,000 max coverage for the year, I have not had to pay anything out of pocket. But what if I need a cavity filled or some other kind of dental work later this year? That, on top of my second cleaning for the year would definitely put my over $2,000 annual max (discussed in this prior article) and I’ll have to pay out of pocket. I’ve done that before, in multiple years. If I’d only been billed in-network rates for all my dental work…I didn’t have the heart to estimate how much I would have avoided paying over the years. I’ve been going to the same dentist since 2007 and have recommended them to many other people. Ugh.

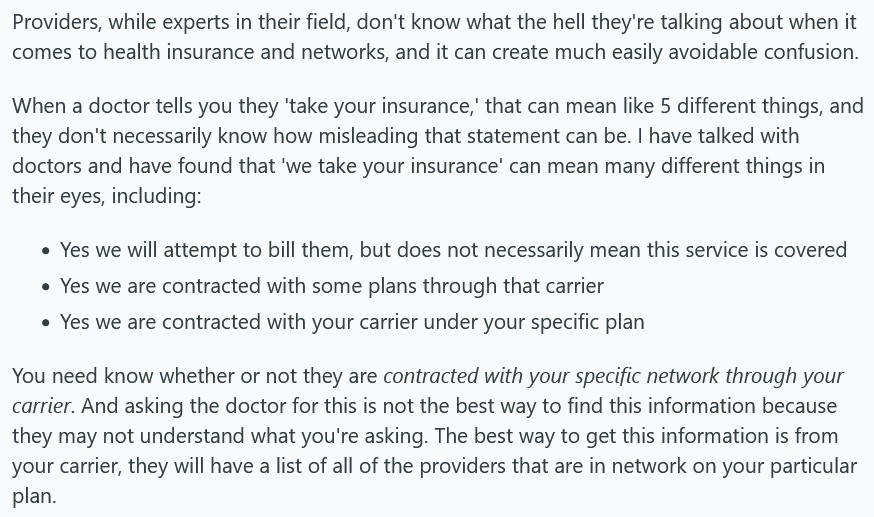

Which brings me back to how the dentist’s office said they “take my insurance.” I thought “we take your insurance” meant they were in-network, but it only meant they’d submit a claim to my insurance company for me. This helpful Redditor elaborates:

Networks can change, so I’d like to think that every dentist in this office, was, at one time, in-network under my particular Cigna dental plan, but…the dentist’s office chose not to bill me that last $100. I looked back and saw that some prior year EOB’s for semi-annual cleanings also show the “Patient Pay” amount as something other than $0. I always understood that my dental insurance fully covered semi-annual cleanings with no deductible, no co-pay, so if I had ever received a bill for a cleaning, I would have immediately known something was wrong and investigated. I think that is why the dentist did not bill me for the balance. They did not want me to go investigating.

Until this year I had never asked my dental insurance company questions like, “What is the in-network rate for an ordinary teeth cleaning?” Or “Was this claim processed at the preferred provider in-network rates? What are those rates?” By not balance billing me, my dentist was able to keep me coming in and continue getting paid at high out-of-network rates. This office always runs perfectly on time and the dentists there don’t push extra dental work, but I am not sure I can stomach going back, even to the one in-network dentist.

-Stephanie

p.s. This is a great time to check that you are up to date on vaccine boosters like measles (more than 1,300 U.S. cases year to date), whooping cough (more than 15,100 U.S. cases year to date), and tetanus. A couple years ago I looked at my records and I was way overdue for tetanus! I’d been getting regular physician checkups, but no doctor had ever checked in with me on vaccines. This summer I got MMR and Tdap boosters and it cost me $0 – no co-pay, no deductible, no payment at all as both were fully covered by my medical insurance. Other adult vaccines to consider are shingles and pneumonia (over age 50) and RSV (over age 60). Could insurance coverage change in the future if, for example, CDC recommendations change? Yes, it could. Go ahead and use that insurance you’ve already paid for.

One reply on “The Boring Newsletter, 7/26/2025”

[…] to pricing. This impacts how much of your annual coverage is used up with each dental visit. I also wrote about how out-of-network dentists may tell you “yes, we take your insurance,” and this also […]

LikeLike