Hi Friendos,

With open enrollment for medical insurance coming up, I’ve been talking about FSAs and HSAs. Last week we looked at quantifying the tax benefit of using an FSA. This week we do it for HSAs. Next week we’ll put it together with choosing a medical plan. If you have questions about this or things you can share from your own strategies, please write in! and I can provide even better info to others.

For HSAs, the financial benefit per year could be anywhere from $1 to about $3,000-ish for “regular” use of an HSA, with the potential for thousands more for “turbo charged” use of an HSA. Today we’ll look at scenarios where things stay the same all year (same medical plan, same job, same spouse if you have one, you’re not about to qualify for Medicare, etc.). These things change all the time but today is for the basics. Then you can build your knowledge in the areas that matter to you.

A health savings account (HSA) is a tax-advantaged account you can use to pay for qualified medical expenses. Once you have money inside an HSA account, that money is all yours, even if you leave your job. Some employers put $ into an HSA account for you. If they do, the money becomes yours as soon as it is inside your HSA account. Inside the account, you can keep the money in cash or invest it in things like mutual funds, like the way you can invest money inside an IRA.

How HSAs work: putting money in (contributions)

You may contribute to an HSA if you have a high deductible health plan (HDHP). Not all medical plans with high deductibles are considered HDHPs, so double check if you’re unsure. Self-employed people can open HSA accounts – they are not just for people with employer-provided health insurance.

In 2023, you can put in up to $3,850 (self-only coverage) or $7,750 (family coverage). If you’re over age 55, add $1,000 to that (catch up contribution). If your employers puts $ into your HSA account for you, that amount does count against your annual contribution limit.

For people with spouses (or domestic partners, if that applies), know that there is no such thing as a joint HSA. An HSA account belongs to only one person and only that person is eligible to contribute to it. If you and your spouse/domestic partner are on a family insurance plan and you both have HSA accounts, the family-level HSA contribution can be split up however you’d like: all to one person’s HSA, all to the other person’s HSA, or some to each, as long as you stay within the allowed total contribution for the year.

How HSAs work: taking money out (withdrawals)

Unlike FSAs, where you can spend your full year’s contribution right away (even though it will take all year for that amount to come out of your paychecks), you can only spend the balance in your HSA at any point in time. If your HSA starts the year at $0 balance, and you contribute $100 per month, you’ll have to wait a while to cover a $500 medical expense you incur in January.

HSA providers may send you a debit card you can use for payment at point of sale. They may send paper checks you can use to pay bills, or let you pay bills online directly from the account. It depends on the account provider. If you pay for something out of pocket, you can reimburse yourself from the HSA account. Sometimes it is easier to pay out of pocket and wait for the dust to settle on insurance administrative stuff so you know the exact final amount you owe for a medical expense.

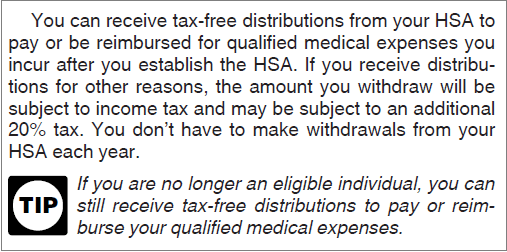

To pay for a medical expense out of an HSA account, the expense must be incurred after you open the HSA account. But you do not need to withdraw from the HSA in the same year you have the medical expense. From IRS Publication 969:

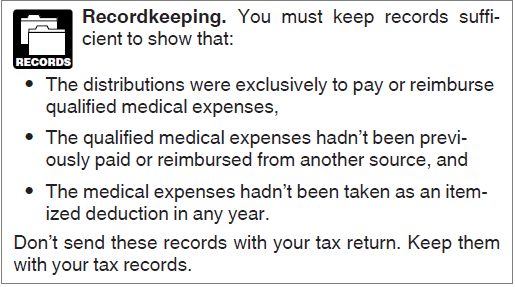

The IRS also provides guidance on recordkeeping, which you’ll want to follow in case you are ever audited by the IRS:

Let’s break that down a little. It sounds like a lot but isn’t so bad:

- #1: Records showing distributions were used to pay only for qualified medical expenses: An EOB (explanation of benefit) from your health insurance plan would be great backup. Itemized receipts that describe what the $ was spent on also work. The purpose of this is to only give tax benefits (discussed more below) for qualified expenses.

- #2: Records showing the medical expenses were not paid or reimbursed from another source: This could be a point-of-sale receipt, a credit card/bank statement showing you paid this, or HSA account statements showing direct payment out of that account. You can scan/take pictures of these and save them electronically, no need to keep the physical paper unless that’s your preference. The purpose of this one is so you don’t double-dip where, say, you actually did have some expense covered and you are also getting reimbursed from your HSA.

- #3: Records showing the medical expenses were not itemized deductions: Your tax returns will show this. You do save copies of those, right? Here too the purpose is to ensure you don’t double dip on tax benefits.

Bottom line: save copies of (1) your tax returns (you want to save those anyway), (2) paperwork showing what the medical expense was for, and (3) paperwork showing that you paid for it.

What’s the $ benefit? (the tax savings)

To receive the full tax benefits from an HSA, you need to use $ for qualified medical expenses. Let’s assume you do that. In that case, the federal income tax savings from putting $ into an HSA are calculated the same way as for FSAs: the amount you put into the account times your marginal tax rate. State income tax savings are also the same, except that for HSAs, California and New Jersey offer no tax savings at the state level.

Let’s say you are single and have a $75k annual salary so are in the 22% bracket for federal income taxes and, we’ll assume, 4% bracket for your state’s income taxes. Every $ you put in an HSA account will reduce your income taxes by 26 cents. If you max your 2023 self-only contribution of $3,850, that saves you $1,001 in taxes (=$3,850 * 26%). For a thousand bucks, I will happily save receipts and organize some paperwork. If you are in higher tax brackets, you save more off your taxes. The more you contribute to the account, the more you save on taxes.

But wait, there’s more! If you contribute to an HSA via payroll deduction, you also avoid 7.65% in payroll taxes (check out the payroll tax bracket tables here). Continuing our example from above, you would save an additional $295 off your payroll taxes (=$3,850 HSA contribution * 7.65%), for a total tax savings of $1,296. Put differently, that’s a tax savings of 33.65 cents for every dollar you contribute to an HSA (=22% + 4% + 7.65%). WOW!

By running your medical expenses through the HSA, what I call “regular” use of an HSA, you can save hundreds or thousands per year.

But wait, there’s even more! If you invest the money inside your HSA account (maybe you choose a nice low-cost index fund) you may never pay taxes on your investment returns. This is what I call “turbo charged” use of an HSA.

Let’s take an extreme example, where someone maxes their 2023 HSA contributions of $3,850 and invests it for 40 years (they manage to cover their medical expenses that year with other $). They can tell their HSA provider: each time I put $ in this account, please have it go into XYZ mutual fund. If we guess investment returns of 7% every year, that $3,850 would grow to $57,652.

In the HSA, if they can use all the $ on qualified expenses, they owe no taxes at withdrawal. Will they really have enough medical expenses that qualify? Probably! Older people usually have quite a few medical expenses, and Medicare premiums and long-term care insurance premiums are “qualified” expenses for HSA purposes.

If that money were inside a 401k, they’d owe income taxes on it at withdrawal, 40 years from now. If tax rates stay the same, that would be $15k (=57,651 * 26%) our example person owes. Now, that’s 40 years from now, so in today’s $ that’s something like $4.6k. Versus $0 for the HSA. This is the additional benefit of leaving $ inside the HSA and investing it. And this example is only for one year’s contribution, but you could do this every year you have a high deductible health plan.

Now, if your alternative to an HSA is putting the $ into a Roth IRA instead of a 401k, or into a regular brokerage account, or something else, the tax comparison #’s will be different, but none of those other options have the possibility of never paying taxes on that income (including perhaps payroll taxes)—only the HSA provides that.

What if you don’t have enough medical expenses to use all the $ in your HSA account? Then after you turn 65, spend it on anything you want and pay taxes at your income tax rate. The HSA turns into a 401(k). You don’t get the extra tax savings, but who cares: you are healthy.

What if you are under 65 and want to spend money in the HSA on non-qualified medical expenses? In addition to paying income taxes, you also pay a 20% penalty. Don’t do that!

If you’re still with me, thank you, I know this one was a slog. Just like American health finance!

-Stephanie

5 replies on “The Boring Newsletter, 10/22/2023”

[…] 100% of our planned spending in the FSA with our traditional plan ($1,500), and, consistent with last week’s discussion, max the HSA contribution with our high-deductible plan […]

LikeLike

[…] HSAs have their own, independent contribution limits. I think of HSAs as a type of retirement account due to the possibility of investing funds that sit inside the account. I discussed this in a prior newsletter. […]

LikeLike

[…] As I have said before, I think of HSAs as a type of retirement account due to the possibility of investing funds that sit inside the account. See this prior newsletter. […]

LikeLike

[…] in the past, explaining how the tax benefit works and quantifying it in dollars (here for FSAs and here for […]

LikeLike

[…] if your job offers an HSA? That money is yours until you spend it, so I personally would count it as savings during the month […]

LikeLike